Swiggy is going full throttle with new revenue streams on the food delivery side, but will this be enough for its $1Bn+ IPO?

Zomato’s food delivery platform is profitable, thanks to platform fees, and Zepto is on a tear on the quick commerce side after raising $1 Bn this year — but both need to thank Swiggy![]()

![]() with at least a hat tip for showing the way.

with at least a hat tip for showing the way.

Swiggy was the first to introduce platform fees in July 2023, and Swiggy Instamart started the quick commerce revolution at the end of 2020. The Bengaluru-based company can take the credit for these two major developments in the Indian consumer internet story.

But now, with its IPO on the horizon, Swiggy not only has to prove its own worth against Zomato but also against Blinkit, Zepto, BigBasket, Flipkart, Jio and others in the quick commerce segment. And this is even before we take a look at the dining out vertical, where Zomato has big plans.

Some clues about Swiggy’s strategy can be seen in this week’s reports about its FY24 numbers. Over the past month or so, it has also launched several new revenue streams. Swiggy is going full throttle ahead of the IPO, but will this be enough to make a bull run in the public markets?

Let’s find out, after these top stories from our newsroom.

- A Messy Split: In the WestBridge vs. Anupam Mittal case, the fate of Shaadi.com hangs in the balance with multiple lawsuits across India and Singapore, and the final resolution could very well shape the future conflicts between investors and founders

- Liquidation Blues: Many noted Indian VC funds will be close to their fund expiry dates in the next 18 months, and SEBI’s updated rules for liquidation with mandatory performance reporting has put these expiring funds under the spotlight. Read to know why

- Did Zomato Overpay? After the high-profile acquisition of Paytm Insider, many industry analysts have questioned whether the INR 2,048 Cr deal price tag was justified or is Zomato stretching itself too much in the hope of building the going-out business

Swiggy Vs Zomato In 2024

It’s all about the IPO. Swiggy’s upcoming IPO is the most anticipated public listing for investors, as highlighted in Inc42’s recent investor survey after H1 2024.

Swiggy, which was last valued at $10.7 Bn, is said to be targeting a valuation of $15 Bn for the IPO where it will look to raise anywhere between $1 Bn and $1.2 Bn. VC and PE giants such as Prosus, Accel, SoftBank and Invesco among others will be looking to cash in on the IPO, which follows a very critical year for Swiggy in terms of proving its revenue scale as well as a path to profitability.

We reported in early 2024 that Swiggy could report over INR 10,000 Cr in revenue for FY24, but it turned out to be much higher than that. According to details from its annual report, the company saw its revenue grow by 36% to INR 11,247 Cr from INR 8,265 Cr in FY23.

More importantly, Swiggy also slashed its net loss by 44% to INR 2,350 Cr during the year under review from INR 4,179 Cr in FY23. Without a look at the audited financials, one can only assume that a lot of the expenses have been incurred as the company expanded its quick commerce network in 2023 and 2024.

The big surge in Instamart quick commerce orders, introduction of platform fees midway through FY24, and growing traction for its ads and dining out business are the platforms that Swiggy is using to attract investors ahead of its IPO.

The company even got a round of minor infusions this past month, with Amitabh Bachchan’s family office, Hindustan Composites, Motilal Oswal Financial Services’ chairman Raamdeo Agrawal joining the cap table recently.

With $1.4 Bn in revenue in FY24, Swiggy’s potential price of $15 Bn in the IPO seems to be justified to a certain extent.

Swiggy investor 360 One, formerly known as IIFL, recently pegged the company’s valuation at $11.5 Bn, with a revenue of $1.4 Bn. In this regard, Swiggy has a lower revenue multiple of just over 10X compared to Zomato’s (close to 20X), thanks to a market cap of $30 Bn. Zomato’s FY24 revenue stood at INR 13,545 Cr or roughly $1.6 Bn.

The biggest factor for Zomato has been it turning profitable on this revenue base. Swiggy is yet to prove that, though it does look like the Bengaluru-based company might turn the corner soon.

What’s Happening With Food Delivery?

For most comparisons, it would be a folly to put Swiggy and Zomato against Zepto directly, as the latter is wholly focussed on quick commerce. For Swiggy and Zomato, food delivery is bread and butter, or it should be, but the rise of quick commerce has come at the expense of slower growth in food delivery volume, at least for Zomato.

Will this also be the case with Swiggy?

By the time Swiggy goes to the public markets, the revenue figure could well be over $2 Bn, especially because the company has structured its main verticals to maximise revenue collection. On the food delivery front, Swiggy has looked to expand revenue streams from both ends.

For consumers, there’s the platform fees as well as Swiggy One subscriptions. It has also looked to make itself indispensable for restaurants.

Within a matter of days in July, the company launched marketing tool ‘Smart Links’ to help restaurants widen online reach and boost orders, as well as a data analytics tool for restaurant partners to gauge their marketing performance against peers. It also rolled out a SaaS suite for partner restaurants to leverage influencer and social media marketing. Then there’s ‘Staffing Support’, an initiative to assist its restaurant partners with staff recruitment.

Most recently, Swiggy launched a large order delivery fleet in metros to compete with a similar offering by Zomato. This fleet is meant to be a way for Swiggy to cater to festive season demand more efficiently.

Sources in the company told Inc42 that for long it has been believed that food delivery is underpenetrated, and if that’s the case, the only way to maximise revenues and profits is to extract more revenue per user. Platform fee has been hiked to INR 6 per order in its key markets, including Delhi and Bengaluru, and this could go even further up depending on how Swiggy sees food delivery growing.

We expect Swiggy to add more premium features for users and restaurants going forward because this is where it is catering to habituated users and app-dependent kitchens. For consumers, using Swiggy can be a discounts-related alternative for Zomato at certain points in time, so offsetting the occasional discounts with per-order platform fee makes sense.

On the restaurant side, Swiggy is looking at cloud kitchens and large restaurants as a growth category. These are the partners who have the most to lose if Swiggy were to suddenly shut its food delivery business. Large restaurants are double-sided partners too, featuring on the Dineout side of the Swiggy revenue menu as well, while cloud kitchens would simply not exist without apps.

And Then There’s Quick Commerce

There is a lot of business rationale in pushing food delivery towards the revenue side and keeping quick commerce towards the growth side. The scope for experimentation is higher on quick commerce right now as the competition is also higher.

With a duopoly on the food delivery side, Swiggy can rest easy in the knowledge that it can’t be blind-sided by a third player. The revenue potential is also way higher for quick commerce in comparison to food delivery, since the former has a higher order frequency per user.

“Quick commerce is the key for long term profitability. Blinkit has already outpaced Zomato’s food delivery business. A Goldman Sachs report this week said that Blinkit’s contribution to Zomato’s market value has surpassed the core food delivery business. So Instamart will be extremely critical for Swiggy,” Rahul Jain, vice president of brokerage firm Dolat Capital, told Inc42 earlier this year.

But Swiggy is also said to be losing ground to Zepto and Blinkit in the quick commerce business. Zepto, which has raised over $1 Bn this year, is gearing up for expansion and is likely to launch 100s of new dark stores across the country this year.

To boost average order value for quick commerce, Swiggy expanded the non-grocery category for footwear, appliances, fashion, beauty and electronics within Instamart. Other players have done the same, and the entry of Flipkart and JioMart is quickly blurring the line between quick commerce and ecommerce.

This will be critical as Zepto claims to be on pace to achieve $1.2 Bn in annual sales in FY24, which will undoubtedly be helped by the recent introduction of Zepto Pass loyalty programme and a per-order platform fee, as well its plans to launch a BNPL-like Zepto Postpaid product.

Zepto is not sitting back when it comes to big plans either, and is reported to be in talks with bankers for an August 2025 date for a public listing.

Even though it remains the second largest quick commerce player in India after Blinklit, Swiggy has seemingly lost its first mover advantage in this category. How deeply will this hurt the Bengaluru-based giant?

What complicates this further is the big push for quick commerce from the likes of Tata-owned BigBasket, which has the category expertise and the scale to compete with Blinkit, Zepto and Swiggy. In fact, BigBasket is merging quick commerce into its main app, which will immediately widen its customer base.

It’s interesting that despite Zomato hitting the public markets before Swiggy, it was not a moment for quick commerce. Swiggy’s IPO will be the first real litmus test of how the public markets embrace the quick commerce model and its revenue trajectory. It’s arguably why the Swiggy IPO is being watched so closely by everyone in the startup ecosystem.

Sunday Roundup: Tech Stocks, Startup Funding & More

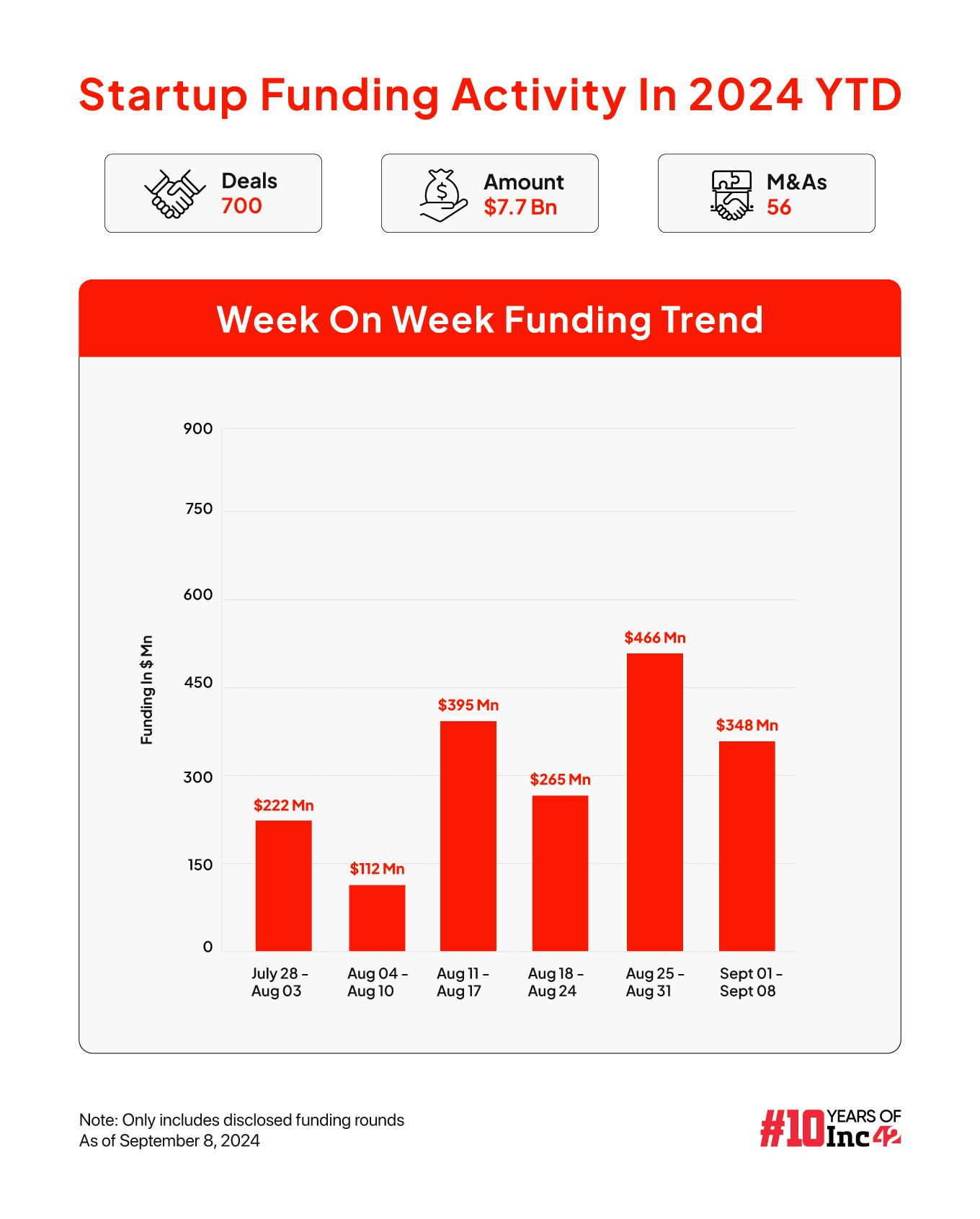

- Mega Rounds This Week: Rapido and Drip Capital led the way with mega rounds as Indian startups collectively mopped up close to $348 Mn in funding across 19 deals this past week

- 30 Startups To Watch: Thousands of early stage Indian startups have featured in our monthly 30 Startups list and this month, we are reaching a new milestone with the 50th edition of our flagship series. Take a peek now

- Rapido’s Unicorn Round: The ride-hailing startup has raised $200 Mn (INR 1,660 Cr) in a Series E funding that catapulted the company into the unicorn club

- EMT’s New Vision: Easemytrip is looking to become a commercial vehicle OEM and incorporated a wholly owned subsidiary Easy Green Mobility to enter electric bus manufacturing

- Another Setback For BYJU’S: The embattled edtech major has seen a second auditor resignation in under a year as BDO stepped down after raising concerns over financial and governance issues

- Ecom Express’s IPO Playbook: After Delhivery’s muted debut in 2022, logistics tech rival Ecom Express is hoping for a different tune as it prepares for its public listing